Welcome to The Growth Factor Fortnightly (TGF Fortnightly). The newsletter explores some of the biggest questions around small businesses through the stories of MSME owners, bankers, investors, customers, employees and technologists.

In this edition

- Raghuram Rajan on reviving MSMEs

- Two SMB lending models for the future

- How MSMs are faring: Good, bad or ugly

- Emergency funds & rescue teams

Raghuram Rajan on reviving MSMEs

In a recent interview with Enquiry, an online show, Raghuram Rajan, former RBI governor, offered some pointers on what to do to revive MSMEs. MSMEs, which accounted for 30% of GDP and employed over 110 million people last year, are among the worst-hit during the pandemic. India's economic growth depends on how well MSMEs perform.

Here are five takeaways from Rajan's interview.

- Increase spending, but spend it wisely: The government is cautious about overspending given the fiscal situation. But, we have to look at the damage being caused by not spending too. We cannot help all MSMEs, but we can objectively choose the entities that are most beneficial to the economy—entities that provide employment, generate profits and pay taxes.

- Engage in constant dialogue: We shouldn’t say, I do this, and wait forever. Instead, it should be “I do this and see what’s the takedown, and then I should do something more.”

- Establish criteria, go with a plan: Some businesses are wary of taking too much debt. But the problem with the government giving equity or grants is that ‘friends and family’ might scoop them, resulting in scandals. So, it’s important to establish clear parameters, and a roadmap.

- Different strokes for different folks: Needs differ. For really tiny MSMEs, the question is how do I get working capital and start up again. They were not borrowing from banks earlier, and so they are not covered under any scheme now. Then there are entities that have loans but can’t go for equity infusion. The question there is debt renegotiation. But this would mean equity infusion into the banks. We have to look at the whole gamut, and not think about it in a piecemeal fashion.

- Sequence reforms: We are like a patient who has been in an accident. The first thing is to stabilise the patient because without that there is nothing to work on. There are other maladies too. We need land, labour reforms. But, we cannot implement reforms that will set back the patient. But there are reforms that don’t do it. Improving the business environment, for example.

Two SMB lending models for the future

In a fintech newsletter from Andreessen Horowitz, Seema Amble argues that models will prevail, both offering loans to SMBs through existing customer relationships.

- Embedded loans, “in which lending is tied to software that the SMB customer already uses as an operating system.”

- The “bank” model, “in which lending is offered in addition to a set of financial products, often starting with a high engagement product like payments or a checking account.”

Both these models, she says, promise to solve three big problems faced by some of the new SME lending firms.

- Distribution problem: Scaling is difficult for small loans because you spend a lot of time and effort acquiring and servicing a small loan, but the returns are much lower compared to big loans. Customer acquisition is tough and expensive.

- Risk selection problem: Lending to SMBs is risky, because many small businesses fold up. The risk is even higher for some new-age lenders because SMBs come to them because they don’t get loans from traditional lenders, community banks.

- Diversification problem: A crisis—such as today’s pandemic—impacts companies across the SMB segment. A lender focused on SMBs faces the brunt during such a crisis, a reason why Kabbage and OnDeck faced problems (and sold to Mastercard and Enova respectively)

Amble gives Stripe and Square as examples, respectively, of embedded loans model and “bank” model (which solves the distribution problem by riding on another service, risk selection problem by having access to more data, and diversification problem by getting only a part of your revenues from lending).

Read the full piece here.

Good, bad or ugly

Teamlease chairman Manish Sabharwal says, with so much uncertainty around, it's hard to tell signals from noise. A single data point doesn't tell much about what's happening on the ground. With that caveat, here are some data points. Ninety percent of MSMEs have started operations post lockdown, but 75% of them are operating at less than half their capacity, according to a survey by National Small Industries Corporation in August. It's better compared to June when nearly 82% of them were operating at less than 50% capacity.

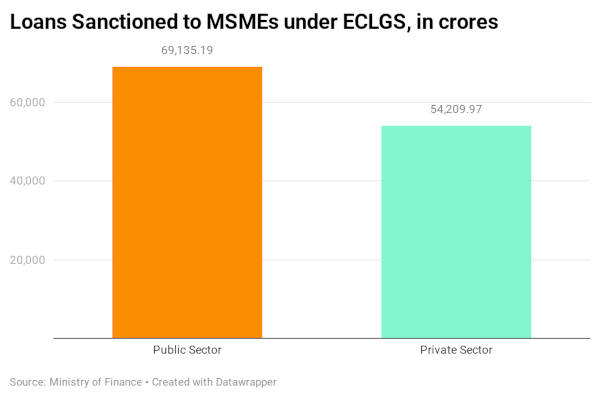

Chart of the week | Emergency funds & rescue teams

By Vasisht Balaji Srinivasan

Much of the government's emergency funds to MSMEs were routed through banks, the traditional medium through which small businesses accessed (or struggled to access) finance. The big question is, how good has the transmission been? This week, let's take a look at the Emergency Credit Line Guarantee Scheme.

https://datawrapper.dwcdn.net/K5Ibz/1/

- Public sector banks sanctioned more funds than private sector banks, which is not surprising because traditionally they were the biggest financiers to MSMEs.

- PSBs have sanctioned about 56% of the total amount, that is Rs 69,000 crore out of a total of Rs 1.23 lakh crore. This means close to 41% of the total amount has been sanctioned in the first four months since the announcement. Is it too slow or about right? Let us know what you think.

- There have been debates around whether the government should have built the capacity to give money to small businesses straight away, instead of depending on banks. The JAM trinity—Jan Dhan, Aadhaar, Mobile—helped the government transfer money straight to the accounts of beneficiaries. What will be the features of a similar infrastructure for MSMEs?

- Even though the government seems to be pumping in money to keep businesses insulated from the crash, the rescue teams have yet to arrive. Only in the latter half of the year (hopefully), when consumption picks up, will businesses be able to get back to, well, let’s call it normal.

Have you availed of credit from the ECLGS? How is it working out for your business? Do write to us and let us know.

All illustrations from Icons8

This fortnightly newsletter is curated by Founding Fuel’s senior writer NS Ramnath, who is researching industrial clusters in Tamil Nadu on a Bharat Inclusion Fellowship. Bharat Inclusion Fellowship, an initiative of CIIE.CO of IIM, Ahmedabad, is aimed at addressing the knowledge gaps that prevent entrepreneurs from developing effective solutions for the underserved.

TGF Fortnightly will share insights from his research and reporting. The newsletter is a part of the conversation we will have with our community—on our website, over video conferences, webinars and a Discourse platform we are setting up. We will keep you posted.

Please do share this newsletter with friends and colleagues who might be interested in this theme. If you received this as a forward, you can subscribe here. Thanks for being a part of what promises to be an incredible journey of learning and insights.