FF Life: The mental accountant

We are hardwired to think of money in multiple categories based on its purpose or context. At the same time, we are naturally afraid of losses of any type. These biases greatly influence our purchasing and investment decisions

18 August 2023· 6 min read

TL;DR

Business leaders seeking to understand financial decision-making will find profound insights into two key cognitive biases: "mental accounting" and "loss aversion." Mental accounting describes our hardwired tendency to categorize money into distinct mental buckets, impacting how we perceive value (e.g., treating a tax refund as "free money"). Loss aversion reveals that the pain of a loss is felt disproportionately more intensely than the pleasure of an equivalent gain, frequently skewing judgment and leading to suboptimal choices. Grasping these inherent psychological patterns is invaluable. It empowers leaders to strategically frame financial communications, optimize product pricing and compensation models, and navigate investment decisions more astutely, ultimately fostering superior business outcomes and mitigating costly psychological pitfalls.

The tax season just went by with millions of taxpayers filing their tax returns. Some will end up paying more tax to the government than their due, and this amount will later be refunded. Do you remember the feeling when the tax refund hits your bank? It is like there is free money to spend.

I have a friend who invests in startups. Last year one of his companies got acquired and he made phenomenal returns. However, another startup investment of his, that I know of, is not going anywhere. My friend is upset that he is about to lose his money in this company. The fact is that he has made over 20x more money in the first startup than what he would lose in the second.

What is happening? How can our mind be fooled like this?

The “mental accounting” bias

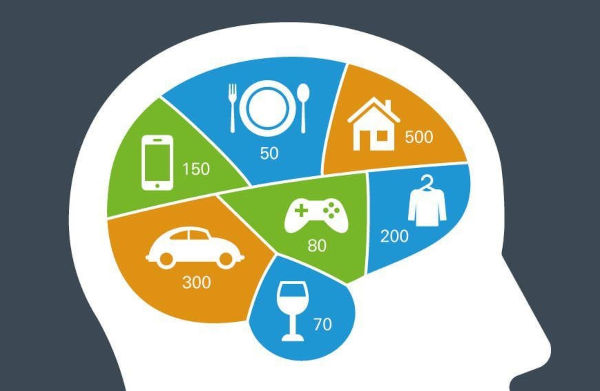

It seems our mind is wired to think of money in different buckets. For each saving, spending or investment, our mind automatically opens a new mental account or ledger. Each such ledger is accounted for and tracked separately, rather than netting it with other accounts.

The tax refund money feels free because in our mind we have already paid the tax and closed that ledger.

[Source: DWS Group on X]

This bias is called "mental accounting" and was first articulated by the economist Richard Thaler, who won a Nobel prize in 2017 for this discovery.

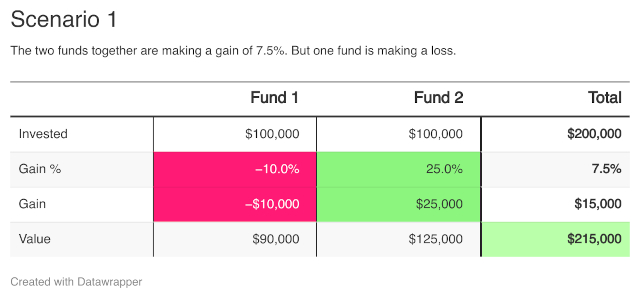

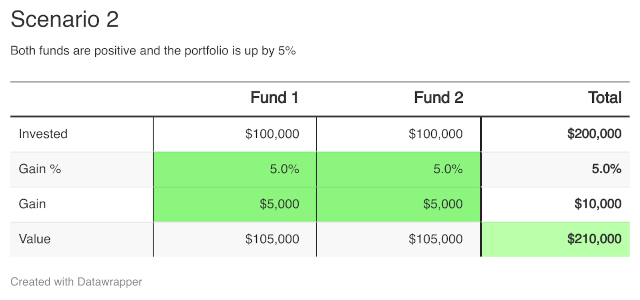

Consider an investor who starts with a financial investment of the exact same amount in two separate funds. Which scenario below would make the investor happier?

The first scenario is clearly more profitable than the second. But, that is not how our mind is wired to think. Since the monies are placed in two separate funds, our mind mentally creates two separate ledgers/placeholders for these funds. The bias is that our mind wishes to evaluate each fund individually rather than netting the profit of one fund with the loss of the other.

Ironically, in the above example, our mental accountant is happier in the second scenario when both funds are individually in the green, even if the total returns are lesser!

“Loss aversion” bias

It is not just that we open different mental ledgers for different heads, but we have a desperate need to be positive in each of the mental ledgers. Our mental accountant is averse to losses of any kind.

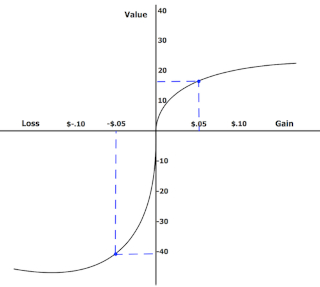

It was Daniel Kahneman and Amos Tversky who first proposed that consumers value gains and losses differently. The same amount of loss has a disproportionate effect on us than a similar gain. We are naturally averse to losses.

[We are likely to be 3x miserable if we lose the same amount that we gained]

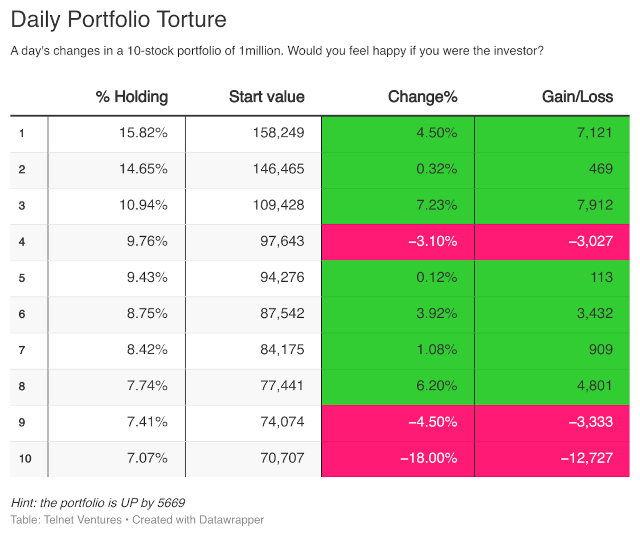

You look at your portfolio on a given day, and see a nice total gain. But, upon drilling into the gainers and losers, you find that one investment is sharply down. This losing investment creates a sharper pang than the overall gain. Effectively, the happiness derived from the total gain is significantly eroded. Loss aversion has spoiled the moment.

The above portfolio is actually up, but that one large losing position is difficult to digest for the mind. The mere presence of the colour red creates a cognitive overload. It is loss-aversion at play.

What explains this mental wiring?

It is the premise of evolutionary theory that none of our traits and behaviours are incidental. The sheer presence of a trait is evidence that it must have helped our ancestors in their survival and hence was selected by natural selection.

The fact that we do mental accounting must certainly have been useful to our ancestors. As early humans evolved millions of years ago, it must have become gradually important to remember interactions with each and every person in the group to be able to reciprocate suitably. The ones who could do this would possibly survive better.

To play the reciprocity game, [humans] need to recognise each other, remember who repaid a favour and who did not, and bear the debt or the grudge accordingly.

– Matt Ridley, The Origins of Virtue

Cognitively, our minds developed to open a separate mental ledger for each person. But the moment it comes to money, our old mammalian minds are confused. Unlike people, money is fungible, i.e. the money from one source is the same as the money from another. The money kept for a vacation is the same as the money saved for education. The money invested in one investment is of the same colour as the money invested in another.

But, our minds are naturally wired to create a new ledger for each and every spending, investment, stock, fund—and we like to evaluate each of them in their own silo.

Our minds are fundamentally incapable of absorbing abstract concepts like money and compound interest, because our ancestors did not encounter these problems in the past.

How does this affect investing?

With a combination of Mental Accounting and Loss Aversion, we have a desperate need to be positive in each of our mental accounts.

This means that when we are selling investments to raise cash, we are far more prone to sell the winners instead of the losers. Selling a loser is unacceptable to our mental accountant. This may explain this famous quote.

Selling your winners and holding your losers is like cutting the flowers and watering the weeds.

– Peter Lynch

Many years back, I was sold Nifty-linked debentures by my relationship manager. These are instruments which offer the upside of the equity index while having 100% capital-protection. Who likes to invest in the capital markets and see the red colour? The result: I made below average returns after three years, but no losses ever! Another instance of our innate loss-aversion exploited by a marketeer. That's why Caveat Emptor. Buyer Beware.

How can we defend ourselves?

Understanding a mental bias does not mean that we suddenly become immune to it. However, being aware of our mental flaw, we can try to construct possible defence mechanisms to counter the negative consequences of these biases.

When selling stocks, we tend to sell the winners instead of losers

Defence strategy:

- List all the stocks on a sheet

- Write one line on each of the companies

- E.g. Infosys could be "Good management. Long-term compounder. Industry headwinds."

- Rank each stock from 0-9, where 9 is maximum confidence

- Sort list by rank. Sell the bottom most stock.

Looking at portfolio, we are prone to focus on the negative

Defence Strategy: Do not look at the portfolio constituents every day!

When buying a new stock, we tend to under-invest

Defence Strategy: When considering making a new investment, think of the total size of the portfolio pie and accord a suitable weight to the new investment. For more, see position sizing.

We naturally gravitate to products that promise capital protection

Defence Strategy: Marketeers exploit our deep aversion to losses to offer attractive "capital-protection" schemes, which offer upside without ever losing the principal capital.

Remember that every investor can create their own capital protection scheme. For Rs 100, keep 90 in a safe investment and invest the balance Rs 10 in a highly risky security (or derivatives!) to achieve the same effect.

We are suckers for buying ULIP and thematic insurance

Defence Strategy: Insurance has always been sold in India mixed with investment. When selling a child education plan, the marketeer is exploiting our mental accounting buckets.

We are always better-off investing in a long-term mutual fund minus the insurance. For life insurance, simply buy a term-plan and nothing else.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Join the conversation

Krishna Jha

Independent investor

Krishna is an independent investor managing a portfolio of both private and public companies.

He is an angel investor in a couple dozen startups while his public portfolio is focused on Indian companies with long-term holding periods.

In his previous avatar he was a technology entrepreneur and his first company was acquired by Infosys spin-off OnMobile.

Website: https://www.krishnajha.com/

Beyond the noise is the signal.

FF Insights: Sharpen your edge, Monday–Friday.

FF Life: Culture, ideas and perspectives you won't find elsewhere — Saturday.

Loading comments...

Readers also liked

·FF Life

FF Life: Beyond the Gate of Conquest

Ramzaan at the Saifee Masjid Complex, in South Mumbai's Bhendi Bazaar: In the heart of chaos, an ode to modernity that embraces the Dawoodi Bohra community's heritage and aspirations

CA

Charles Assisi

Co-founder and Director | Founding Fuel

FF Life: Beyond the Gate of Conquest

Ramzaan at the Saifee Masjid Complex, in South Mumbai's Bhendi Bazaar: In the heart of chaos, an ode to modernity that embraces the Dawoodi Bohra community's heritage and aspirations

Co-founder and Director | Founding Fuel

·FF Life

FF Life: The Oscar Rosters 2025

A review and breakdown of the nominees of the main categories of the 2025 Oscars and their chances of winning

RR

Ronaan Roy

Former Deputy General Manager | Mahindra

FF Life: The Oscar Rosters 2025

A review and breakdown of the nominees of the main categories of the 2025 Oscars and their chances of winning

Former Deputy General Manager | Mahindra

·FF Life

FF Life: The rewards of writing

It’s a window to learning, making connections, and a form of personal riches

KJ

Krishna Jha

Independent investor

FF Life: The rewards of writing

It’s a window to learning, making connections, and a form of personal riches

Independent investor

Explore more

Dive into other themes from our network.