The Economy We Have, Not the One We Imagined

Why the Gulf crisis may be India’s moment for the next phase of reform

24 March 2026· 15 min read· 3 comments

TL;DR

This incisive analysis reveals India's economic reality diverges sharply from its perceived image. The Gulf crisis has starkly exposed that a decade of 'app-economy' growth, while convenient, masked foundational weaknesses: stagnant manufacturing, and a services-led model unable to lift a vast workforce from low-productivity agriculture.

For business leaders, this moment is a critical inflection point. The external shock, by removing the 'fog of inaction,' compellingly triggers deep structural reforms. This signals a potential re-engineering of India's economy, pivoting from superficial convenience to robust industrial capacity. Understanding this strategic pivot is crucial for informing investment decisions, anticipating market shifts, and identifying new opportunities as India builds a more resilient and inclusive foundation.

Editor's Note

This essay builds on Haresh Chawla’s earlier Trendspotting 2026 essay on India’s growth model. Written in the context of a fast-moving geopolitical shock, it revisits that thesis with new evidence and sharper questions on the path ahead.

In January 2026, I argued that India cannot app its way to prosperity—that a decade of platform capitalism had built a dazzling convenience layer while leaving the middle engine of growth floundering. I was right about the diagnosis. What I did not anticipate was that the pressure needed to act on it would arrive so fast, and so forcefully.

New evidence now suggests that India’s GDP growth may have been systematically overstated for over a decade. The economy now confronting a Persian Gulf on fire is not the one we thought we had.

Because policymakers can now see the economy we actually have clearly. The fog that sustained comfortable inaction has lifted. And the external shock, brutal as it is likely to be, has done what no think-tank paper or opposition motion could: it has made the cost of the status quo undeniable.

The rupee has slid past 93 to the dollar. Fertiliser prices are rising sharply just as the kharif season approaches. LPG supply has been disrupted because natural gas from Qatar, which declared force majeure last week, has stopped flowing.

This is not a scenario. This is happening now.

The war may end and the immediate shock may pass. LPG cylinders will be available again. Workers in Surat will return.

But what this moment leaves behind is harder to ignore.

The fires are burning in the Gulf. The powder keg is here.

This pressure in India’s political economy has historically been the only reliable precondition for reform. The question is whether we use this one. This piece is an attempt to say that clearly, before the crisis forces the wrong answer.

A Layer, Not a Foundation

In my January Trendspotting essay, I argued that India’s digital decade had delivered convenience without prosperity, aggregation without capacity, and market-cap cycles without national progress. The evidence since has only strengthened that argument. The war has made it urgent.

But beneath that convenience layer, structural foundations were being weakened—on both sides. The demand side was compressed by stagnant wages and consumption sustained increasingly through debt. The supply side was constrained by bureaucratic friction that made investment progressively harder to justify, regardless of demand signals.

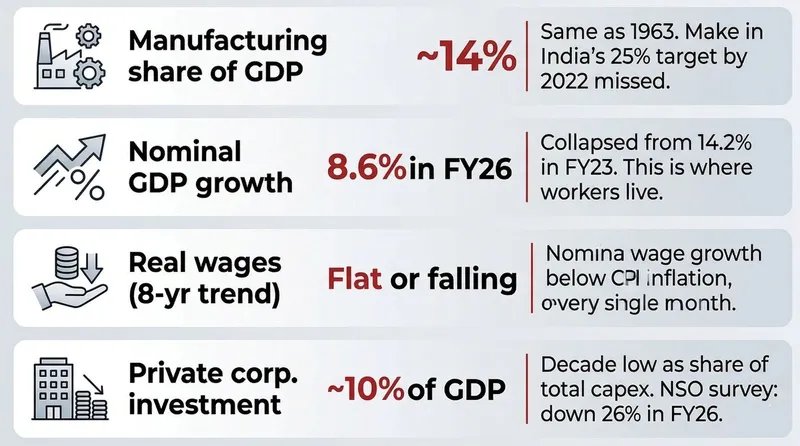

The manufacturing data serves as its own indictment. “Make in India” was launched in 2014 with the vaulting ambition of raising manufacturing’s share of GDP to 25% by 2025. Yet, a decade later, the needle has not moved.

In FY24, manufacturing’s share of GDP stood at about 14%—a figure virtually identical to the one recorded in 2013–14, and among the lowest levels seen in the modern era. Despite ten years of policy effort, the macro-level structure of the economy remains frozen.

The human cost is even clearer in the labour statistics. Manufacturing remains a minor player in the national labour market, stubbornly accounting for only about one in ten Indian jobs. This stagnation stands in stark contrast to the 46% of the workforce still tethered to agriculture.

The “Skipped” Phase: Every Asian success story—South Korea, Taiwan, China, Vietnam—built its middle class by moving workers from farms to factories. India is caught in a skip of this essential manufacturing phase, leaping prematurely into a services-led model that cannot absorb mass labour.

The result is a staggering productivity mismatch: nearly half the country is locked in a sector that generates less than one-fifth of GDP. Without a manufacturing engine to pull millions out of low-productivity farming, prosperity remains a narrative of the few, while the many remain stuck in the fields.

India’s manufacturing stagnation is also a structural consequence of proximity to China. Indian manufacturers are not losing to a better competitor. Chinese manufacturing benefits from subsidised credit, export rebates, clustered supply chains, and logistics scale that compress production costs well below market benchmarks. India’s trade deficit with China has only been increasing every year, with manufactured goods flowing one way. Production Linked Incentive (PLI) schemes attempt to build capacity at market cost against that subsidised scale. But without addressing input tariffs, scale, and capability, the gap cannot close. Much of India’s value addition remains assembly of parts made elsewhere.

To put it simply: you cannot have 1.4 billion consumers without creating commensurate income-earning jobs. Without jobs, there is no demographic dividend. There is demographic drag.

The platform decade monetised the top, lent to the middle, and scrolled past the rest. This is the structural inheritance the economy carries into the Hormuz crisis.

You cannot have 1.4 billion consumers without creating commensurate income-earning jobs. Without jobs, there is no demographic dividend. There is demographic drag.

But structural inheritance is not structural destiny. And a crisis that forces the diagnosis to the surface is, at minimum, the beginning of the cure.

Capex Without Conviction

Private corporate capital expenditure—the kind that builds factories, creates jobs, and expands productive capacity—has fallen to a decade low as a share of total investment. The National Statistics Office’s (NSO’s) survey of private corporate capex intentions suggests companies plan to cut a further 26% in FY26.

Corporate India has the strongest balance sheets in fifteen years. Cash flow from operations to capex stands at 1.6x—companies are generating more cash than they are deploying in India. The capital exists. The conviction to deploy it does not.

India’s bureaucratic friction between investment intent and execution remains punishing: land acquisition that can take years, environmental clearances that move at the pace of government correspondence, input tariffs that make manufacturing uncompetitive before it begins, and contract enforcement so slow that disputes outlast business cycles. Each of these raises the hurdle rate on investment.

But even if friction is removed, weak demand still prevents capacity creation. Firms do not build for markets that are not growing in volume terms.

The two blockages reinforce each other. Weak demand reduces the incentive to invest. Weak investment suppresses wage growth. Suppressed wage growth, in turn, weakens demand further.

Fix only one side, and the other prevents recovery. That is the trap.

The diagnostic clarity now available to policymakers is itself a precondition for the reform that follows. The two-sided blockage—friction on supply, weakness on demand—is precisely what a two-sided reform can address. The diagnosis, for once, matches the prescription.

Borrowing to Stand Still

If investment is being squeezed from both sides, so is the Indian household. The K-shape is nowhere more visible than in housing.

Premium real estate has been on a multi-year tear. Luxury launches in Mumbai, Delhi-NCR, and Bengaluru set records in FY24. Prices in prime micro-markets have appreciated 40–60% in three years. Developers have responded by shifting supply toward higher-ticket projects, where margins are more predictable and buyers less price-sensitive.

Affordable housing—the most reliable indicator of whether prosperity is actually broadening—tells the opposite story. Launches in the below-₹40 lakh segment have stagnated or declined as a share of total supply.

Developers have moved away from this segment not because demand does not exist, but because it does not exist at price points that make projects viable. Rising land costs, regulatory overheads, and construction inputs require ticket sizes that flat incomes cannot support. The result is a market where need and affordability have drifted apart.

If you want to understand whether India’s prosperity is broadening, don’t look at the Nifty. Ask whether a household earning ₹40,000 a month can buy a home in most Indian metros or major cities. For years, the answer has increasingly been no.

The savings and debt data show what this feels like from inside that same household.

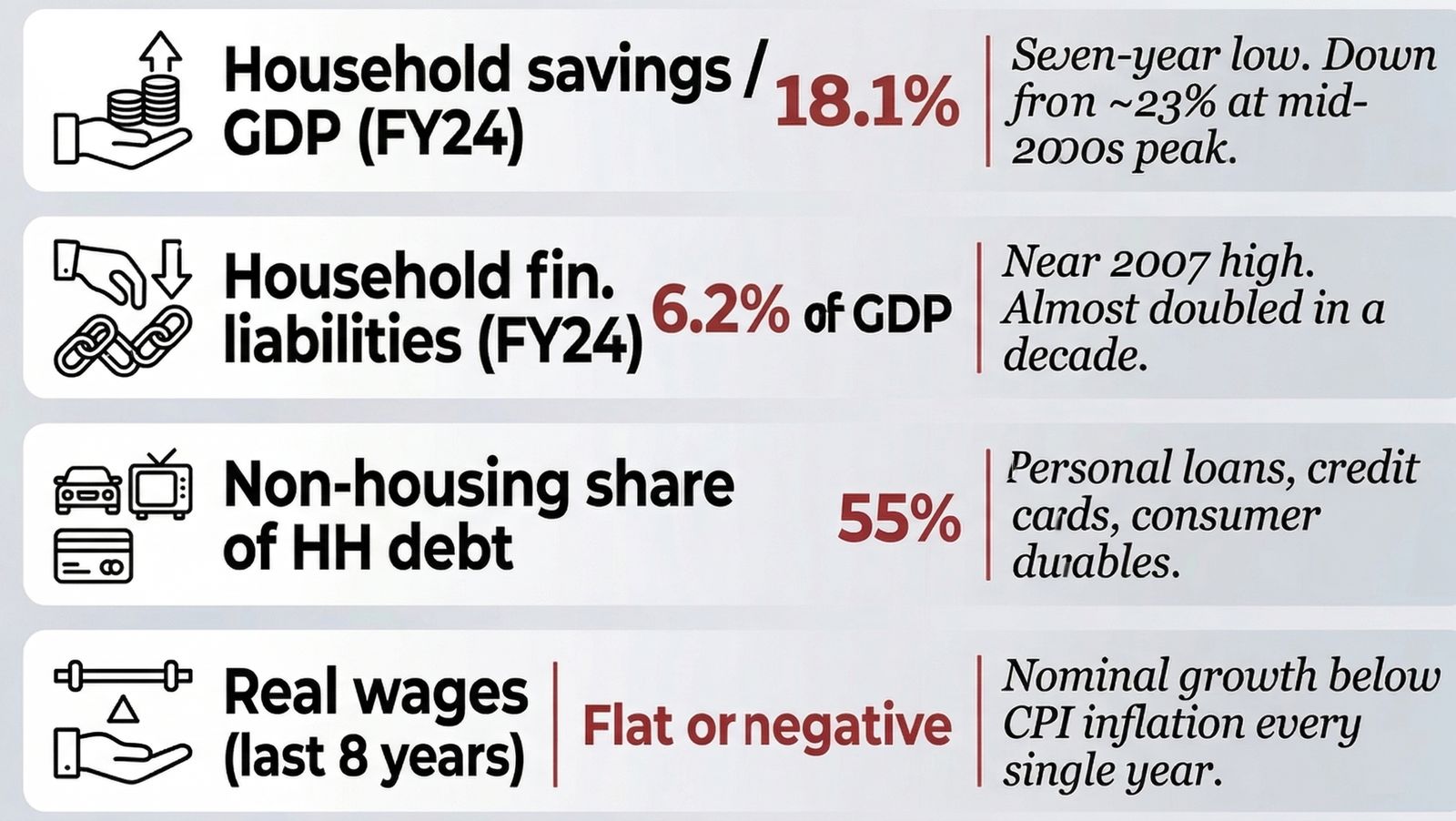

Household savings have fallen for three consecutive years to 18.1% of GDP—a seven-year low. Gross domestic savings have declined from 32.2% of GDP in FY15 to 30.7% in FY24. On the other side of the ledger, financial liabilities have surged to 6.2% of GDP, nearly double the level of a decade ago.

Households are not just borrowing more, they are also saving less. That combination matters.

A household that is saving less and borrowing more is not investing in its future. It is smoothing its present.

The composition of that borrowing is even more revealing. The 55% non-housing share of household debt points to a shift away from asset-backed borrowing toward unsecured or short-tenure credit—personal loans, credit cards, consumer durables financing. This is borrowing to sustain consumption, not to build assets.

Households with rising incomes borrow against assets—housing, education, productive capacity. Households with stagnant incomes borrow to maintain a standard of living that wages no longer support.

A household that is saving less and borrowing more is not investing in its future. It is smoothing its present.

This is what it means, at scale, to run to stay in place.

Credit, in this context, is not the engine of growth. It is the painkiller.

The corporate-level data reflects the same reality. When HUL—a company built to serve India’s mass market—pivots to premiumisation as strategy, it signals something fundamental.

Premiumisation is what you do when the mass market stops growing. When small packs and ₹10 sachets no longer grow in volume, you sell a ₹400 variant to the top 15% and call it growth. Across mass FMCG, margins have been managed through cost rationalisation, grammage reduction, and input adjustments. Volume growth has been far less robust than headline value growth suggests. The constraint is not competition. It is purchasing power.

This is the demand ceiling that Rathin Roy identified in a recent The Economic Times column—India’s growth looks strong on paper, but demand tells another story.

India’s growth model has served the consumption of the top decile—roughly 140 million people—while sustaining the rest through subsidy-induced spending. The economy has not produced, at competitive prices without subsidy, what the next 400 million want to buy.

Private investment stagnation is both a response to this demand environment and to the friction costs of investing at all.

Standstill manufacturing. Investment without conviction. Households borrowing at the peak.

The topline GDP number looked healthy. Everything beneath it pointed in the other direction.

The Fog Machine

If this structural deterioration was real and measurable, why didn’t we see it?

Three forces provided cover.

The first was digitisation. UPI, Jan Dhan, and the formalisation of retail through QR codes improved participation and increased income velocity. India’s working capital cycle shortened. Money moved faster. Transactions became frictionless. Small businesses entered formal networks. Cash leakages reduced.

But digitisation improved the movement of money, not the creation of income. It increased velocity without expanding the base. It made existing incomes travel further and circulate faster, but it did not create new incomes at scale.

This distinction matters.

An economy can feel more active—more transactions, more payments, more visible activity—without becoming meaningfully richer. Velocity can mask stagnation. When money moves faster, it creates the appearance of expansion even when underlying incomes are not growing proportionately.

The second was the post-COVID spending surge. Three years of suppressed consumption were released into eighteen months of extraordinary demand across 2022 and 2023. Households that had deferred spending during lockdowns began to spend simultaneously—on travel, housing upgrades, consumer durables, discretionary consumption.

Every sector appeared to boom.

But this was not the beginning of a new cycle. It was the release of a backlog. A temporary expansion mistaken for a structural shift.

Treating that surge as a new baseline led to overestimation of demand strength by firms, by markets, and by policymakers.

The third, and most powerful, was financialisation.

Equity markets surged. Demat accounts multiplied. Retail participation deepened. Premium real estate reached extraordinary valuations. The wealth effect for the top 20% of urban households was real, visible, and large.

But financialisation did more than create wealth. It changed perception.

Rising asset prices created a sense of prosperity that extended beyond the segment experiencing it. Consumption at the top end began to dominate aggregate numbers. Luxury housing, premium consumption, discretionary spending—all surged.

People felt richer. They spent accordingly.

But a wealth effect is not the same as rising incomes.

Asset price appreciation is episodic and uneven. Income growth is structural and broad-based. The former can create bursts of consumption. The latter sustains it.

In India’s case, the two were conflated.

Asset price appreciation looked like prosperity. It was not wages rising, factories being built, or the middle of the pyramid moving up.

The K-shape concealed this effectively. Aggregate consumption looked healthy because spending by India One—driven by asset gains—dominated the averages. The stagnation of the mass market, the weakening of affordable housing, and the compression of the purchasing power of the bottom half of the population were all averaged out into something that resembled moderate growth.

The fog held.

What is now visible wasn’t visible two years ago. You cannot reform what you cannot see clearly.

Now the Fog Clears

That fog is now lifting and each of the mechanisms that sustained it is beginning to reverse, almost simultaneously.

The Nifty has corrected from its highs. The wealth effect that drove discretionary consumption is now working in reverse. Falling portfolios change behaviour. People spend less, even if incomes have not changed. The adjustment is psychological before it becomes financial.

SIP flows—which at their peak channelled over ₹30,000 crore a month into equities—are likely to slow as first-time investors encounter losses. The cohort that entered markets between 2020 and 2024 experienced four years of near-continuous gains. Many are now flat or underwater for the first time. For a generation of investors, this is the first real drawdown. The confidence that drove incremental consumption is weakening.

A strengthening dollar accelerates the adjustment. In periods of global stress, capital moves to safety—US treasuries and the dollar—and away from emerging markets. Foreign portfolio investors have been net sellers of Indian equities for several months. The result is a feedback loop: falling markets, a weakening rupee, and rising import costs.

The demand that came from asset inflation—not income growth—is now deflating, just as oil and fertiliser shocks hit from the other side.

And then there is FPI behaviour—often explained away as rotation.

Over the past five to seven years, foreign portfolio investors have been persistent net sellers of Indian equities, with cumulative churn—buying, selling, and reallocating—running into several lakh crore rupees. The net outflow is smaller, but the direction is consistent.

The convenient explanation is relative value—money moving between markets. That explanation is too easy.

FPI capital is not sentimental. For years, they extended India’s growth story the benefit of the doubt. They stayed invested through volatility. They priced in future earnings. What they were measuring, quietly and consistently, was the gap between narrative and earnings.

That gap did not close.

Corporate earnings growth did not keep pace with expectations embedded in valuations. Consumption remained uneven. Investment did not accelerate. The broadening that should have followed headline growth did not materialise.

A strong story can sustain premium valuations for a while. Over time, if the story does not translate into earnings, the premium compresses—and capital exits.

This was not rotation. It was a patience trade.

And the patience ran out.

The fog did its job. It persuaded enough.

The fog that sustained comfortable inaction has lifted. The cost of the status quo is now undeniable.

The most dispassionate readers of the data were less convinced. Now, as markets correct and the external account comes under pressure, the last mechanism sustaining the illusion of broad-based prosperity is unwinding.

The gauze is coming off the wound.

What the GDP Was Hiding

If the fog distorted perception, the data now raises a more uncomfortable possibility: that we were not just misreading the economy, but mismeasuring it.

The distinction matters. A misreading can be corrected with better analysis. A mismeasurement requires revisiting the assumptions that underpin policy itself.

What looked like a strong economy may, in fact, have been a weaker one all along—with implications that are only now becoming visible.

In March 2026, Abhishek Anand, Josh Felman, and Arvind Subramanian published India’s 20 Years of GDP Misestimation: New Evidence, presenting a provocative case: India’s growth has been systematically overstated for over a decade.

At the heart of their critique is the deflator—the statistical tool used to strip inflation out of nominal growth to arrive at “real” growth.

The logic is simple: if the economy produces ₹100 of goods this year and ₹108 next year, has it truly grown by 8%? Not if prices also rose by 8%. In that case, actual output is stagnant. The deflator is the “price correction” that reveals the truth.

In India’s current cycle, this calculation has reached a historic divergence: Nominal GDP growth (the raw rupee value of the economy) has tumbled from 14.2% in FY23 to a projected 8.6% in FY26.

Yet, official real GDP growth remains remarkably resilient, pegged at 7.6%.

The divergence between these figures suggests an implied deflator that appears unusually low relative to the inflation households and firms actually experience. This suggests that across the entire Indian economy, from services to manufacturing, prices are barely moving. While statisticians might attribute this to falling wholesale commodity prices (WPI), it simply does not align with the lived experience of the Indian consumer or business owner.

This is more than a technical debate; it is a fundamental policy issue. We are measuring success in “real” terms while the economy people actually inhabit—the one that dictates wages, corporate revenues, and debt servicing—has slowed sharply.

The nominal economy is where people live. When the nominal anchor slips this far, “real” growth begins to feel like a statistic rather than a shared reality. If we misdiagnose the actual “heat” in the economy, we risk prescribing the wrong medicine for India’s future.

If growth is overstated, policy is calibrated to a reality that does not exist. Interest rates may remain tighter than needed. Fiscal choices may assume a resilience that is not there. Reform urgency may be underestimated because the system appears to be performing better than it is.

Mismeasurement does not just distort perception. It delays response.

And in an economy where both demand and supply are already constrained, delayed response compounds the problem.

If this interpretation holds, the economy is materially smaller than we believed. The consumption base is narrower. The investment base is weaker. The tax base is thinner.

Two forces are at play.

The first is domestic demand weakness—visible in wage stagnation, premiumisation, and the compression of mass consumption.

The second is global manufacturing overcapacity—particularly from China—suppressing prices across traded goods.

Solving one does not solve the other.

It is the specification for what Reform 3.0 must be.

The Bill Arrives

The war is now imposing four simultaneous reality checks.

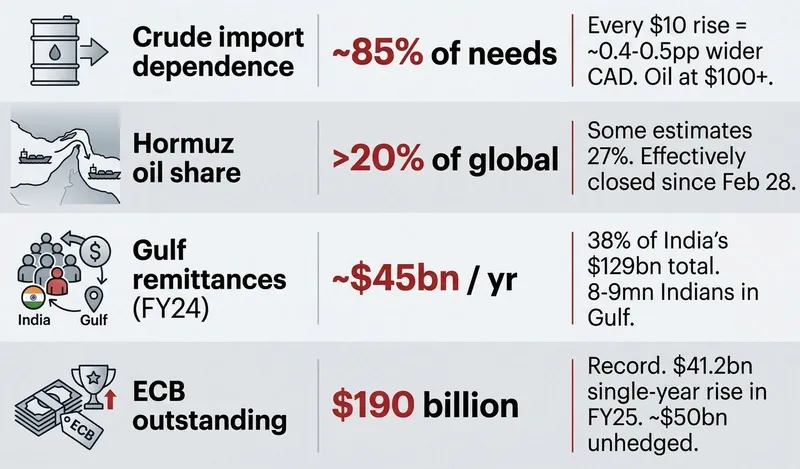

The first is oil. With the energy import bill expanding materially, India’s Current Account Deficit could move toward roughly 2% of GDP or somewhat above if elevated oil prices persist—placing fresh pressure on the rupee just as global capital flows turn more cautious.

This adjustment is not abstract. It is transmitted directly through fertiliser costs, transport, and the cost structure of the entire economy. Diesel prices affect logistics. LPG affects household budgets. Fertiliser costs feed into food inflation. Each layer passes through to the next.

The households absorbing this shock are already financially stretched.

The second is remittances. India receives well over $100 billion annually in remittances—the largest inflow globally—with a large share coming from the Gulf economies. For millions of households across Kerala, Karnataka, Uttar Pradesh, Bihar, Andhra Pradesh, and Rajasthan, this is not supplemental income. It is core income.

Remittances do not sit idle. They fund consumption, education, housing, and local economies. Any disruption—through layoffs, wage compression, or return migration—feeds directly into demand in some of India’s most densely populated states. The effect is immediate and local.

The third is fertilisers—the least discussed and most immediate impact.

India imports a large share of its fertiliser inputs, including urea, phosphates, and potash, with significant dependence on the Gulf. With supply chains disrupted and input costs rising, domestic producers have already begun cutting output. Emergency procurement is underway, but timing matters.

The kharif sowing season does not wait for policy response.

Fertiliser shortages or price spikes at this stage do not just affect farm economics. They affect yields, incomes, and rural demand months later. This is a delayed shock embedded in the next cycle.

Farmers, already operating on thin margins, now face input costs they cannot absorb—for inputs they may not be able to source.

The fourth is services, where the shock is not just cyclical, but structural. India’s $250 billion IT and ITES export sector, long insulated from commodity shocks, now faces pressure from two directions.

Geopolitics is slowing discretionary tech spending globally. Clients delay projects, reduce budgets, and stretch decision cycles.

At the same time, AI-driven efficiency gains are reducing the need for entry-level service roles—the very segment that powered employment growth over the past two decades. What was once a scalable employment engine is now becoming more output-efficient but less labour-intensive—a structural shift that predates the crisis, but becomes more visible under it.

Underlying all four is the external commercial borrowing (ECB) exposure. At approximately $190 billion, with a significant portion unhedged, a rupee in the 92–95 range creates balance sheet stress for firms with dollar liabilities.

A weaker rupee also feeds directly into imported inflation—raising the cost of fuel, edible oils, electronics, and other essentials—further compressing the purchasing power of households already under strain.

This is not just a currency movement. It is a transmission channel into corporate balance sheets—and potentially into the banking system through credit risk.

In 1991, one shock met one weakness.

Today, multiple shocks are hitting an economy already flagging on both demand and supply fronts.

But simultaneous shocks concentrate political attention. Every item on this list has a corresponding policy lever.

1991: The Seductive Parallel

Every time India faces external pressure, 1991 is invoked—the idea that crisis forces reform.

But the comparison is misleading.

In 1991, the constraint was primarily on the supply side. The reform prescription was clear and the world agreed on it: open the economy, remove the controls, let competition in. Manmohan Singh had a ready toolkit. And it worked, because the license-raj economy had suppressed entrepreneurial energy waiting to be released. Remove the lid, and the pressure did the rest.

Liberalisation worked because it matched the constraint.

Today’s economy has two simultaneous constraints.

On the supply side: bureaucratic friction—land, clearances, tariffs, enforcement—that raises the cost of investment.

On the demand side: a structural ceiling—flat real wages, a narrowing consumption base, and households borrowing to sustain spending.

A 1991-style response addresses one constraint and worsens the other.

Supply-side reform without demand creates capacity without customers. Demand stimulus without supply leaks into imports.

Half a reform is worse than none.

India needs both sides addressed together.

The Reform We Actually Need

The solution is not difficult to describe. It is difficult to execute.

Remove the barriers to investment—land, clearances, tariffs, contract enforcement. At the same time, expand the purchasing power of households so that demand exists for what is produced.

Expanding purchasing power is not a single lever. It is a set of choices.

It could mean strengthening rural incomes through agricultural productivity and infrastructure, rather than price support alone. It could mean enabling MSMEs—where most employment sits—to pay higher, more stable wages through easier access to credit and lower compliance friction. It could mean targeted income support that sustains consumption without distorting incentives.

The mix can be debated. The direction cannot. Do one without the other, and the system fails.

Interest rates are the most direct connector. Lower rates reduce the cost of capital for firms and the debt burden for households. The RBI has begun easing, however temptation to follow war-led inflation may force it to reconsider, which may be counterproductive.

The harder question is fiscal quality.

There is a number that dominates every budget discussion, every rating agency report, every IMF consultation. The fiscal deficit. Get it below 4.5%. Then 4%. Then 3.5%. The assumption baked into this obsession is that a smaller deficit is always better. It is the wrong question entirely.

If we borrow to build cold chain infrastructure, fund real schools, or lay industrial corridors, that is an investment that pays back with interest. If we borrow to announce free electricity before an election, or fund a loan waiver that is simply spending tomorrow’s money to buy today’s votes—that is a different thing entirely.

The question is never how big the deficit is. The question is what it is building. Fix the corruption that hollows out every rupee before it reaches its destination. Make public spending productive. Repair the relationship with corporate India so government investment pulls private investment in rather than substituting for it. Do those things, and a larger deficit is not a burden. It is a bet on the future.

If anything, our tax and GST collections are strong. The issue is allocation.

An increasing share of spending is directed toward transfers that generate electoral returns but do not build capacity—free power, loan waivers, pre-election cash transfers. These provide relief. They do not compound.

Investment in public goods—education, agricultural infrastructure, skills—creates lasting productivity. The distinction is clear. The trade-off is unavoidable.

India cannot afford both.

This is where the political economy becomes binding.

Transfers are visible, immediate, and electorally rewarding. Investments in public goods are slow, diffuse, and politically under-credited. The incentives, therefore, are misaligned with the outcomes the economy needs.

Reform, in this context, is not just about identifying the right policy mix. It is about sustaining choices whose benefits are delayed and whose costs are immediate.

That makes the sequencing harder. It also makes the window narrower.

The longer the system relies on consumption support without expanding productive capacity, the harder the eventual adjustment becomes.

And then there is the jobs problem.

For two decades, services absorbed millions into formal employment. That ladder is now being eroded from the bottom by AI. Entry-level tasks are being automated.

This would be manageable if a manufacturing base existed beneath it. It does not.

The rung above is weakening. There is nothing below to catch the fall.

None of this is difficult to understand. It is difficult to implement.

Closing

Unlike 1991, India is not broke. It is something more workable than that: an economy whose real constraints are now visible to everyone who needs to act on them.

The GDP mismeasurement debate, the investment stagnation, the household debt surge, the manufacturing plateau—none of this was hidden. It was averaged out, smoothed over, and obscured by a fog that served too many interests. That fog has now lifted, not gradually, but in a single season of shocks that has left no room for comfortable re-reading of the data.

That is actually the prerequisite for reform. India in 1991 did not reform because it found wisdom. It reformed because the comfortable alternative had been removed. The same logic applies today. With one critical difference. In 1991, the prescription was known and the only task was to implement it. Today, the prescription itself must be more sophisticated: supply and demand must move together, and fiscal quality must replace fiscal quantity.

The hard part is not knowing what to do. The hard part is choosing to do it before the next election cycle offers a reason to defer. Indian history suggests that governments act boldly when the cost of inaction exceeds the cost of reform. We are at that threshold.

The Gulf has given India a mirror. What we do next will determine whether we act on what we now cannot unsee.

A question for readers:

What, in your view, is the binding constraint today—demand, supply, or the political economy of reform?

Share your thoughts in the comments below. Haresh will respond to as many as he can.

Join the conversation

Haresh Chawla

Investor | Entrepreneur

Haresh Chawla is an investor, entrepreneur and business builder with over three decades of experience across media, consumer businesses and the digital economy in India.

He currently invests independently in consumer, food and digital businesses, working closely with founders and management teams to help build and scale enduring companies.

He also serves as a visiting faculty at SPJIMR where he teaches a course that lies at the intersection of Digital Transformation and Entrepreneurship.

Previously, Haresh was a Partner at True North (formerly India Value Fund Advisors), one of India’s most respected private equity firms, where he focused on investments in the food and consumer sectors and worked closely with management teams to transform and scale mid-sized businesses.

He is widely recognised for his role in building and transforming the Network18 Group into one of India’s most influential media networks. As Founding CEO, he led Network18 through a period of extraordinary growth, turning it into India’s fastest-growing media and entertainment company. Over a 12-year tenure, he scaled revenues from $3 million in 1999 to over $500 million in 2012.

In his dual leadership roles across Network18 and Viacom18, he helped create a multi-platform media conglomerate reaching more than 300 million households across television, print, film, mobile and digital. Under his leadership, the group expanded from a single TV production business into India’s leading multimedia network with over 11 television channels, including Colors, CNBC-TV18, CNN-IBN, MTV India and Nick India. He also forged landmark partnerships and joint ventures with global media leaders such as NBC (Comcast), CNN, Viacom, Forbes and A&E Networks.

Haresh has been closely associated with India’s consumer internet evolution since its early days and has played a role in building several of the country’s most recognised digital platforms, including Moneycontrol and BookMyShow.

He continues to mentor and invest in emerging consumer and technology ventures.

Earlier in his career, he was part of founding teams at HCL Comnet; ABCL, where he set up the film distribution business; and the Times of India Group, where he launched Times Music.

Haresh holds a Bachelor’s degree in Engineering from IIT Bombay and a Master’s degree in Business Management from IIM Calcutta.

Beyond the noise is the signal.

FF Insights: Sharpen your edge, Monday–Friday.

FF Life: Culture, ideas and perspectives you won't find elsewhere — Saturday.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Loading comments...

Readers also liked

·Economy, Policy & Society

Reform 3.0: Why India Keeps Missing the Mountain

India didn’t falter for lack of ideas or ambition. It faltered because too many parts of its economy were never aligned toward the outcome that mattered most—productive work at scale.

HC

Haresh Chawla

Investor | Entrepreneur

Reform 3.0: Why India Keeps Missing the Mountain

India didn’t falter for lack of ideas or ambition. It faltered because too many parts of its economy were never aligned toward the outcome that mattered most—productive work at scale.

Investor | Entrepreneur

·Economy, Policy & Society

We Passed the Exam. We Failed the Economy

On how India built its education system faster than it built the economy to absorb it

HC

Haresh Chawla

Investor | Entrepreneur

We Passed the Exam. We Failed the Economy

On how India built its education system faster than it built the economy to absorb it

Investor | Entrepreneur

·Economy, Policy & Society

The US–Israel War on Iran: The Risks to India’s Strategic Hedging

Energy dependence, remittance flows and trade corridors reveal how deeply India’s economy is tied to stability in West Asia. Part II of a two-part series.

VK

Vivek Y. Kelkar

Researcher, Analyst & Columnist on Geo-economics, Geopolitics and Sustainability

The US–Israel War on Iran: The Risks to India’s Strategic Hedging

Energy dependence, remittance flows and trade corridors reveal how deeply India’s economy is tied to stability in West Asia. Part II of a two-part series.

Researcher, Analyst & Columnist on Geo-economics, Geopolitics and Sustainability

Explore more

Dive into other themes from our network.