[Gautam Adani (left), by Chirag200201 (CC BY-SA 4.0), via Wikimedia; Prannoy Roy, by World Economic Forum (CC BY-NC-SA 2.0), via Flickr. Images cropped from original]

(Editor’s note: This story was updated on December 6, and December 24, 2022. If you’ve read the story already you can jump straight to the December 6 update by clicking here, and for the December 24 update by clicking here.)

By the time you read this, the end game on Adani’s NDTV takeover may not be entirely over—but there would be enough pointers towards a swift closure.

On Saturday, November 26, the securities trading ban imposed by markets regulator SEBI on Prannoy and Radhika Roy ended. It would inevitably prompt Adani, the current owners of the shell company Vishvapradhan Commercial Pvt Ltd (VCPL), to submit its request—for the second time—to RRPR, the holding company of the Roys, to convert the warrants and issue RRPR shares, amounting to 29.18% stake in NDTV. The request is most likely to be issued as early as possible this week.

The first time the Adanis made this request on August 23, the Roys had returned the money citing a set of constraints that prevented them from going ahead with the warrant conversion. So in effect, if the Adanis hoped for a swift transfer of control, that didn’t happen. Yet they still decided to go ahead and filed the open offer with SEBI for an additional 26% stake in NDTV, without holding a single share of NDTV.

It was interesting to see how SEBI would deal with this piquant situation. It was probably the first time that such a situation had come to the surface. In normal course, the takeover would have been triggered after Adani acquired 26% in NDTV or agreed to do so. And that didn’t happen. Since the Roys had maintained that their consent, under the terms of the 2009 loan agreement, was not sought in writing, technically, the second condition also remained unfulfilled.

The status reports on the open offer available on the SEBI site shows there were a set of letters exchanged between the markets regulator and JM Financial, the merchant banker to the issue, but the specifics are not available in the public domain. The chances are that SEBI may have relied on the 2009 loan agreement to clear the open offer. After all, SEBI’s stated position since 2019 has all along been that, given the structure of that loan, it triggered an open offer back then. Except that SAT subsequently overturned the ruling. In continuation of that stance, SEBI filed an appeal over the SAT order with the Supreme Court in October. However, the hearings have been adjourned twice. The next hearing is likely in about four weeks’ time.

On Friday, November 11, SEBI cleared the formal letter of offer, which in turn also confirms that the Adanis’ warrant conversion is yet to be consummated. The moot point is whether the markets regulator ought to have waited till the warrant conversion was completed, after the trading ban on the Roys got automatically lifted on November 26. Clearly, they did not feel the need to wait and allowed the tendering process under the open offer to start on November 22. We’ll come to the tendering process in a bit.

It is useful to bear in mind that the Roys now don’t have any legal reasons for not going ahead with the warrant conversion. In the first week since the Adanis announced their momentous decision to buy out the Reliance-Nahata stake in VCPL, the Roys had raised a few issues that they said prevented them from carrying out the transfer. One, in 2019, SEBI had placed a securities trading ban on the Roys for lack of proper disclosures around their 2009 loan agreement with the Ambanis. The Roys had then argued that the ban prevented them from carrying out the warrant conversion. That is now no longer tenable. Also, the Adanis had swiftly produced a letter from the Income Tax department clarifying that the IT department had no objection to the warrant conversion, yet another issue that the Roys had brought out.

The beginning of the end

Once the warrant conversion happens this week, the end game will have truly begun. In the meantime, the tendering process is equally intriguing. The open offer price of Rs 294 is well below the current market price of around Rs 406. Therefore, there is no incentive for public shareholders to tender in their shares at that price. Yet a little more than 53 lakh shares, amounting to around 31% out of a maximum offer quantity of 1.67 crore shares have been tendered, according to the last update on BSE at 4:00 PM on Monday. Who are these investors and why did they tender their shares? There is no way to know the identity of these shareholders, till the tendering process ends on December 5.

Before the warrant conversion, the Roys could have played one last card: invoke the Ministry of Information and Broadcasting (MIB) guidelines on the licence on uplinking and downlinking. According to clause 3.1.2 of the MIB guidelines, permission would be granted to a broadcaster, only in cases where equity held by the largest Indian shareholder is at least 51% of the total equity. The Roys could have argued that the warrant conversion would reduce their stake in NDTV from 61% to 32%, and make them non-compliant with the MIB guidelines. If that was their last bargaining chip, specific amendments issued by the MIB on November 9 have significantly diluted the Roys’ bargaining powers. This was adroitly done by not diluting the core guidelines, but through amendments that force higher standards of disclosure from NDTV, including making it mandatory to submit any loan agreements that the broadcaster may have entered into. Now, that would make it mandatory for NDTV to submit the loan agreement RRPR may have entered into with VCPL. Without getting caught in the weeds, these amendments would thus create an opportunity for the Adanis to claim their legitimate co-ownership of NDTV.

What options are the Roys left with?

So what’s next? Over this last weekend, FT published an interview with Gautam Adani, where he spoke about his responsibility to maintain NDTV’s editorial integrity. And more importantly, he also stated he had invited Dr Prannoy Roy to stay on as chair of NDTV.

How the Roys respond to this overture remains to be seen. For Adani, this move signals an attempt to play down any public concerns around a hostile takeover of a big media entity. For Roy to stay on as chairman of NDTV, even while the operating reins pass on to Adani, may not be an acceptable arrangement. Unless there are clear commercial benefits for the Roys in doing so.

In any case, as soon as the warrant conversion goes through, the Roys no longer have to worry about the outstanding interest-free loan of Rs 403 crore in RRPR, since the ownership of the holding company will now lie with the Adanis. Plus, they don’t need to worry any more about the shares that are attached with the Income Tax authorities either. Both provide compelling reasons for the Roys to go ahead with the warrant conversion.

On December 5, if one assumes that the Roys decide not to tender in their shares and the warrant conversion goes through, they will still retain their 32% stake in NDTV, even after the open offer ends.

It also remains to be seen how the Adani open offer fares. The worst case scenario is that they end up with an additional 8% stake from the open offer, if some of the body corporates like Kolkata-based Drolia Agencies, Confirm Realbuild and GRD Securities and Mumbai-based Adesh Broking, and large resident individuals holding significant stakes in NDTV, sell their stake. (See the latest public shareholding of NDTV here.) The best case scenario is that they mop up around 22% shares of NDTV. That could happen if Vikasa India EIS and LTS Investments, the two foreign portfolio funds rumoured to be close to the Adanis, choose to tender their shares before the open offer ends. The two FIIs hold 4.42% and 9.75% stake in NDTV, respectively. So if the warrant conversion goes through and the open offer yields an additional 22%, the Adanis could easily cross 51% stake.

For Gautam Adani, the success of the open offer is more about prestige and avoiding a loss of face. Either way, the Adanis will have greater control over NDTV by the time the open offer ends. Once their stake is higher than the Roys, they could push for a motion to be deemed as the promoter group. And also make drastic changes to the board composition. If Vikasa India EIS and LTS Investments don’t tender in their shares, they could still provide outside support to the Adanis.

Where does that leave the Roys? One, what if Dr Prannoy Roy is unwilling to stay on as chair, essentially a figurehead role? His wife Radhika and he could look to exit by selling their 32% stake in a block deal to a set of institutional investors through a secondary market placement.

With the Adanis emerging as a dominant force in India’s business firmament, there may be enough appetite among institutional investors to mop up a large chunk of floating stock in an Adani group company. For instance, last week, according to a story published in The Morning Context (the story is behind a paywall), LIC, the state-owned life insurer, had invested Rs 78,000 crore in the group in the last two years.

However, pending tax issues have been hanging like a Damocles’ sword over the Roys. While the exact tax claims are hard to verify, sources say, including penalties, the dues are likely to be in the region of Rs 800 crore. That’s not all. On November 11, NDTV disclosed to the bourses that the Central Bureau of Investigation had disallowed the sale of 20% stake in Malaysian media and entertainment group Astro Awani Network. The company said it was considering its legal options.

Here’s the nub. If their continued stint at NDTV and proximity to the powerful billionaire industrialist Gautam Adani, known to be close to Prime Minister Narendra Modi, helps in any way bury the hatchet with government agencies (CBI, ED and Income Tax authorities) and buys them long-term peace, it could be an option that the Roys are likely to seriously consider.

(This is an expanded version of a column that first appeared in Business Standard)

Update: December 6, 2022

It is widely believed that the conclusion of the Adani open offer for an additional 8.26% stake in NDTV marks the end of the final chapter in this three-month-long takeover battle.

Shortly after the Roys concluded the warrant conversion and issuance of shares to Adani in RRPR, amounting to 29.18% indirect stake in NDTV, on November 29, NDTV was required to mandatorily inform the MIB about the change in NDTV’s shareholding pattern. Hence, it is safe to assume that the MIB has been made aware about the loan agreement.

Now, this is a significant development for the Adanis.

Let’s look at what’s transpired since last Friday. The Adanis tried to establish their bonafides to be included as part of the promoter group at NDTV, along with the Roys. This was done by a disclosure to the bourses. That this move was straightaway rebuffed by NDTV through its own disclosure went largely unnoticed in the media.

NDTV even went to the extent of “mauling” the prescribed SEBI format, thereby creating a piquant and extraordinary situation where the two disclosures for the same transaction were radically different. (See page 6-7 of the NDTV disclosure).

Through their disclosure, NDTV tried to pull off three things: One, it refused to acknowledge the indirect acquisition, instead calling it an “indirect vestiture”. Two, it refused to name Vishvapradhan Commercial Pvt Ltd (VCPL) as an acquirer, which the Adanis have clearly done. And three, the Roys have referred to the 2009 and 2010 loan agreements, which the Adanis have not referred to.

In effect, the Roys have simply created grounds for a possible challenge, if the two parties do not see eye-to-eye.

So will the Roys smoke the peace pipe or will they refuse to blink and rebuff Gautam Adani’s overture to have Prannoy Roy stay on as chairman? The answer may emerge in the next one month or so.

Either way, the scenario on what the Adanis could do next has been laid out, like this story in Business Standard clearly lays out.

“As the largest shareholder, the Adani group can propose reconstitution of the NDTV board,” Sriram Subramanian, managing director, InGovern, a Chennai-based proxy advisory firm, said. Prannoy Roy is the chairperson of NDTV, while Radhika Roy is the executive director, according to BSE data.

“For this, the Adani group will have to call for a shareholders’ meet and propose new directors on the board. This proposal will have to be put up for voting by shareholders, which will be an ordinary resolution requiring 50 per cent of voting shareholders to approve it,” he said.

The fact is that the Adanis are now undeniably the single largest shareholder at NDTV. And they hold all the cards.

The chances are that the Roys and the Adanis could arrive at a negotiated settlement. However, if the Roys don’t bury the hatchet and vote against any motion that the Adanis bring up at the shareholders meet, it could in effect deny them an opportunity to walk away with a negotiated settlement.

However, the Adanis have a fall back option. If the two foreign portfolio investors, LTS Investment Fund and Vikasa India EIF Fund, which collectively hold a 14.17% share in NDTV, sell their stakes to an Indian entity, the Adanis could combine their 37% stake with that Indian entity to push through any changes they seek at the board.

Whether the Adanis will be forced to do so, would depend entirely on their ability to persuade the Roys to smoke the peace pipe. The next few weeks will tell us how this long-drawn takeover saga could end.

Correction: We had wrongly assumed that the new MIB guidelines issued on November 29, 2022 were “amendments” to the MIB guidelines of 2011. They, in effect, had completely overridden the 2011 guidelines, which stipulated, among other things, that the single largest Indian shareholder in NDTV–namely the Roys–needed to hold a minimum of 51% stake at all times. The critical 3.1.2 clause has now been dispensed with. This story has been updated to reflect the changes.

Update: December 24, 2023

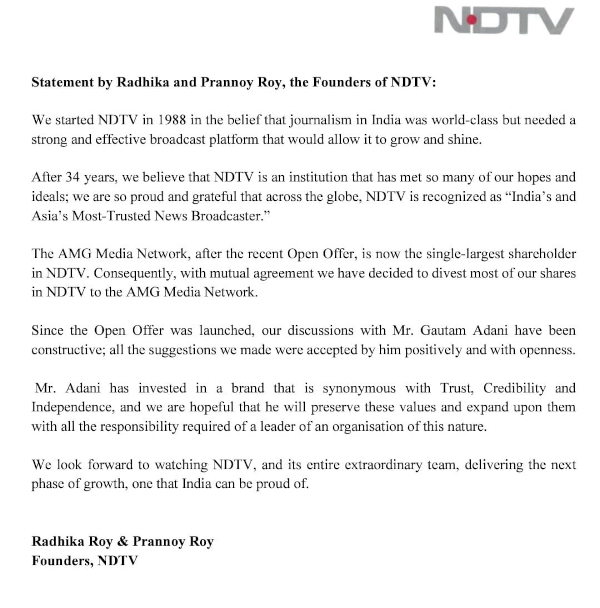

The much awaited deal is done. The Roys have effectively signed off as NDTV founders, having announced their intent to “divest most of their shares” to AMG Media Network, a wholly owned subsidiary of the Adani group.

NDTV shared a letter from the Roys disclosing their intent to almost fully exit from the broadcasting company they founded 34 years ago. (see below)

It brings the curtains down on a takeover battle that stretched over four months. It generated considerable public interest—and sparked heated debate about corporate ownership of media and the role of independent media in one of the largest democracies in the world.

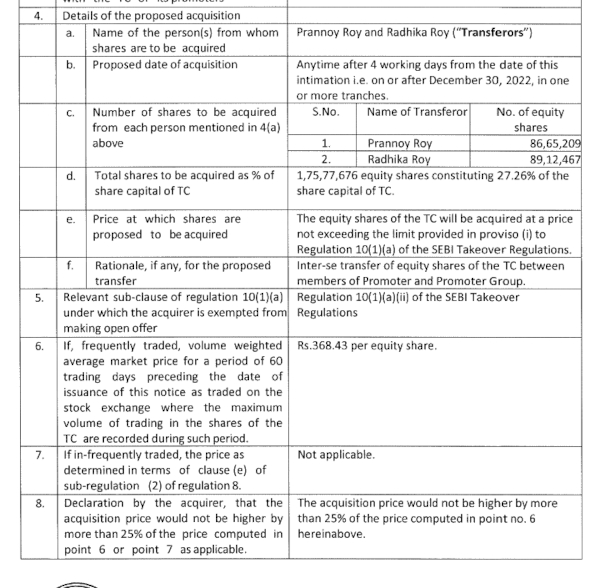

NDTV confirmed that the Roys had sold their combined stake of 27.26% in NDTV, leaving a residual stake of around 5%. In a disclosure to the bourses, NDTV has also informed that RRPR has disclosed the details of the transaction, as it is bound to do so under the SEBI Takeover Code. According to the disclosure (see below), RRPR has confirmed that it will stick to a price that “would not be higher than than 25% of the computed price” prescribed under the Takeover Code. In effect, since the computed price is Rs 368.43 per equity price, the upper limit of the price that the Roys could potentially receive is around Rs 460 per share. If that is the maximum strike price allowed under the Takeover Code, the Roys could potentially earn around Rs 808 cr for selling their 27.26% stake.

NDTV also announced that its board met on Friday to also approve the appointment of two additional directors nominated by the board of promoter entity RRPR Holding. The additional directors were Sanjay Pugalia and Senthil Chengalvarayan who were appointed in the capacity of non-executive, non-independent directors, NDTV said in its disclosure to the bourses.

There is yet no communication on whether the Roys will continue on the NDTV board. In his interview to the Financial Times, Gautam Adani had invited Prannoy Roy to chair the board.

Update (Jan 16, 2023): Media reports confirm the Roys were paid around Rs 603 crore for their 27% stake. Meanwhile, there have been exits from NDTV's management team, and staff has raised queries at the first townhall over editorial freedom after the takeover.

Correction (Jan 16, 2023): A reference to uncertainty over how the Income Tax claims get settled by the Roys, has been deleted. The claims will not matter. Because it will now fall upon the Adanis to handle it since they own RRPR.

{kind=link}