Fintech Special Report Part 1: Indian fintech at a crossroad

The outlook for fintech companies has shifted from unchecked optimism to uncertainty. The rose-tinted glasses are off and some of the well-funded companies are pivoting. Their future will depend on their ability to look beyond technology as the panacea. Part 1 of a 4-part series

10 August 2023· 6 min read

TL;DR

Indian fintech, once marked by unchecked optimism and billions in VC funding, is now at a critical juncture. The initial focus on rapid scaling and technology as a panacea has been challenged by market saturation, regulatory hurdles, and disappointing public valuations for even prominent players like Paytm.

The key insight for business leaders is that success demands more than just innovation. Sustainable differentiation and a profound understanding of human behavior, often overlooked by purely algorithmic approaches, are paramount. Companies are strategically pivoting to profitable models, like Instamojo's shift to SaaS, or seeking new avenues for growth beyond core financial products. This evolution underscores a maturing market where strategic foresight and genuine value creation will define long-term viability, moving beyond mere growth hacking.

Indian fintech used to be marked by optimism

Even a few years ago, there was tremendous optimism about the fintech industry in India. Many believed that fintech companies were on an unstoppable rise, growing their user base, introducing innovative products, capturing market share, and enabling financial inclusion in India.

Venture capitalists poured billions of dollars into Indian fintech, egged on by rosy reports from analysts and consultants. Companies such as Paytm, PhonePe, PolicyBazaar and Razorpay were constantly making headlines as they secured huge investments and became unicorns, companies with over a billion in valuation. Some of them went public.

The industry's focus was on scaling up. Fintech entrepreneurs and the VCs who funded them believed that the hard problem of showing that technology worked for finance had been solved. Now, it was only a matter of expanding the market. “Our job is to find and fund entrepreneurs who can hack growth,” a VC declared at that time.

The optimism has now been replaced by concerns about fintech’s future

However, in the past couple of years there has been a serious rethink. The exuberance that defined the mood of the fintech industry melted away. Some of the well-funded companies that were betting on the segment are pivoting, or at least hedging their bets, either because they see the landscape without the rose-tinted glasses of yesteryears or because those glasses have been snatched away from them by the harsh reality.

For example, even back in 2018, Instamojo, which raised funds from Kalaari Capital, Mastercard, and AnyPay for its payments gateway business, realised that the road ahead was going to be tough and pivoted to a SaaS model for e-commerce, helping direct-to-customer services. Since then it has become profitable.

Similarly, Niyo, a company founded by two ex-bankers from Standard Chartered and Kotak Mahindra and funded by Accel, has now expanded to launch a travel tech platform. Its founders explained that its core products were no different from what other companies offer: “Niyo could do something to gain an edge but how much can someone differentiate a normal savings account?” one of the co-founders said.

Lending has always been core to banking and finance and held a huge promise for fintech. But digital lending has been one of the hardest hit, by regulations and the reality of the market. For example, ZestMoney, a leading buy-now-pay-later company with investments from Goldman Sachs, Omidyar Network, and Zip, found itself in a corner as losses mounted. It tried to sell itself to BharatPe (which itself has fallen into tough times), Pinelabs (which is doing better), and finally to PhonePe (a decacorn, owned by Walmart thanks to its acquisition of Flipkart). It looked like the deal would go through, but PhonePe pulled back saying the company failed their due diligence. ZestMoney laid off over 100 people and is now trying to turn itself into a SaaS player.

Companies that went for IPO are trading at a discount. Paytm, which started trading on stock exchanges in November 2021, is selling at less than half its IPO price. PolicyBazaar is down by 33%. Others such as Mobikwik which was planning for an IPO are postponing it.

The industry is currently at a crossroads

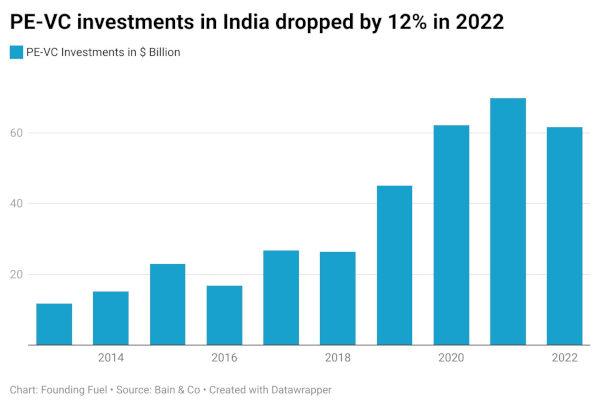

These examples reflect the broader struggles of fintech players. Among all the unicorn fintech companies, only one, RazorPay, is making a profit. VC investments which kept the fintech companies afloat, are saving their dry powder. The number of deals and the size of investments in the fintech sector fell by over 50% in 2022. VC investments dropped by over 70% in the first half of 2023. While companies were fighting for talent during the height of the pandemic, there have since been hiring freezes and even layoffs. At least 650 people were fired last year from fintechs according to a Longhouse Consulting analysis for The Economic Times.

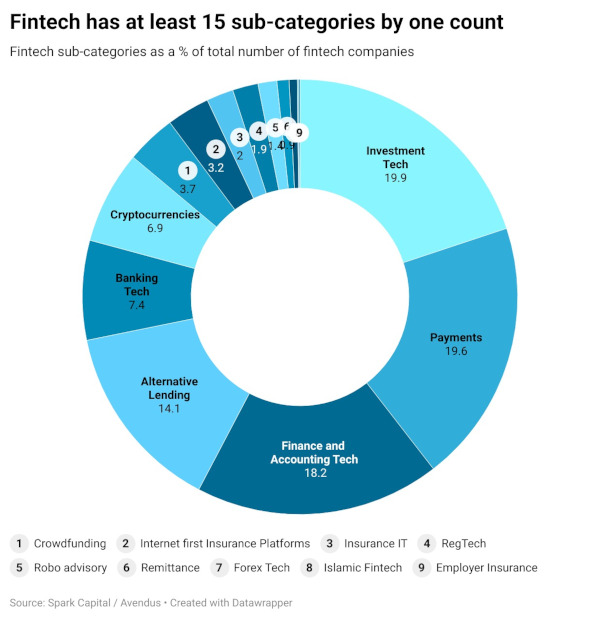

Now, exuberance has been replaced by introspection. As a result, the future of fintech will not be a scaled-up version of what is there today. It will be different. There is already a range of fintechs — enterprise, consumer-facing, payments, lending, insurance, wealth management, advisory, etc. — today, each with its own characteristics.

Some will change much more than others, but the future will be different for all. "It's part of the evolution of Indian fintech," says Ram Ramdas, co-founder of Wonderlend Hub, a digital credit gateway platform. "We are right in the middle of the first and second phase of that evolution."

The shape of its future depends on three factors: a) its partnership with established players; b) its willingness and ability to look beyond technology; and c) its relationship with regulators.

How the industry shapes up in the coming years depends on three factors.

First, how well the incumbents and challengers are able to work with each other, rather than against each other. About ten years ago, the dominant narrative was that the nimble new players will eat the incumbents such as banks and non-banking financial companies (NBFCs) for lunch. The playing field seemed to be in favour of the challengers. It has changed since then, thanks to a number of reasons, including the path India took to developing the basic digital infrastructure. Now, many have started talking about collaborations and partnerships, rather than competition.

Second, how well technologists can make room for “buggy humans in a messy world” (as the title of the newsletter of a value investor puts it), even as they use technology. For many technologists, and by extension, for Fintech startups, it is a matter of faith that more data and better algorithms can replace human effort. This is the way to bring down costs and take finance to new markets, they believe. This was one of the reasons for optimism about fintechs. Now, some of that is turning into scepticism. Financial data is incomplete. The use of alternative data often throws up spurious correlations. There is a growing realisation that technology can’t yet replace people on the ground, and it’s hard to capture the complexities of human behaviour with algorithms. Techies have to work a lot more with fuzzies before the benefits reach people at large.

Third, how well the ecosystem finds the balance between regulation and innovation. VCs and entrepreneurs want to focus on innovation. RBI is focused on customer safety and systemic stability. In the past, many fintechs have tried to push the system towards innovation, even if it comes at the cost of customer safety and systemic stability, and the RBI has asserted its authority every time. As this continues, the big question is how much fintechs can innovate, while ensuring it's aligned with the two big goals of the regulator.

How the industry deals with these three issues is important

While fintech has come a long way in the last ten years, the road ahead is still long. How fintech impacts the world of finance, business and society at large will depend on what’s happening on the ground right now.

We’ll cover the ground reality in Part 2 of this special report, as fintechs realise they need to collaborate, not compete, with incumbents.

Read all 4 parts here.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Founding Fuel is sustained by readers who value depth, context, and independent thinking.

If this essay helped you think more clearly, you may choose to support our work.

Join the conversation

N S Ramnath

Senior Editor | Founding Fuel

NS Ramnath is a member of the founding team & Lead - Newsroom Innovation at Founding Fuel, and co-author of the book, The Aadhaar Effect. His main interests lie in technology, business, society, and how they interact and influence each other. He writes a regular column on disruptive technologies, and takes regular stock of key news and perspectives from across the world.

Ram, as everybody calls him, experiments with newer story-telling formats, tailored for the smartphone and social media as well, the outcomes of which he shares with everybody on the team. It then becomes part of a knowledge repository at Founding Fuel and is continuously used to implement and experiment with content formats across all platforms.

He is also involved with data analysis and visualisation at a startup, How India Lives.

Prior to Founding Fuel, Ramnath was with Forbes India and Economic Times as a business journalist. He has also written for The Hindu, Quartz and Scroll. He has degrees in economics and financial management from Sri Sathya Sai Institute of Higher Learning.

He tweets at @rmnth and spends his spare time reading on philosophy.

Beyond the noise is the signal.

FF Insights: Sharpen your edge, Monday–Friday.

FF Life: Culture, ideas and perspectives you won't find elsewhere — Saturday.

Loading comments...

Readers also liked

·Business & Strategy

Fintech Special Report Part 2: From competition to collaboration

The ground reality has changed. Fintechs are realising that partnerships and ecosystem thinking are key to winning the market, not competing with the incumbents. Part 2 of a 4-part series

NR

N S Ramnath

Senior Editor | Founding Fuel

Fintech Special Report Part 2: From competition to collaboration

The ground reality has changed. Fintechs are realising that partnerships and ecosystem thinking are key to winning the market, not competing with the incumbents. Part 2 of a 4-part series

Senior Editor | Founding Fuel

·Technology & the Future

Fintech Special Report Part 3: The limits of algos

Fintechs bet on data and algos to know the credit-worthiness of the underserved. However, there's a gap in what the data can reveal because of consumer behaviour. Part 3 of a 4-part series

NR

N S Ramnath

Senior Editor | Founding Fuel

Fintech Special Report Part 3: The limits of algos

Fintechs bet on data and algos to know the credit-worthiness of the underserved. However, there's a gap in what the data can reveal because of consumer behaviour. Part 3 of a 4-part series

Senior Editor | Founding Fuel

·Economy, Policy & Society

Fintech Special Report Part 4: A fine balance

Fintech must contend with inherent conflicts with what the regulators want. Fintech’s push for rapid scaling needs to balance with the regulators’ push for financial stability and consumer protection. Part 4 in this 4-part series

NR

N S Ramnath

Senior Editor | Founding Fuel

Fintech Special Report Part 4: A fine balance

Fintech must contend with inherent conflicts with what the regulators want. Fintech’s push for rapid scaling needs to balance with the regulators’ push for financial stability and consumer protection. Part 4 in this 4-part series

Senior Editor | Founding Fuel

Explore more

Dive into other themes from our network.